Types of Working Capital – Complete Guide for MSMEs

Types of Working Capital – Complete Guide for MSMEs

Working capital is the backbone of any business. It ensures smooth day-to-day operations such as paying suppliers, managing salaries, maintaining stock levels, and covering regular expenses. However, working capital is not a single concept. It is classified into different types based on duration, nature, funding structure, and business usage.

Understanding the types of working capital helps business owners choose the right financial strategy and funding option.

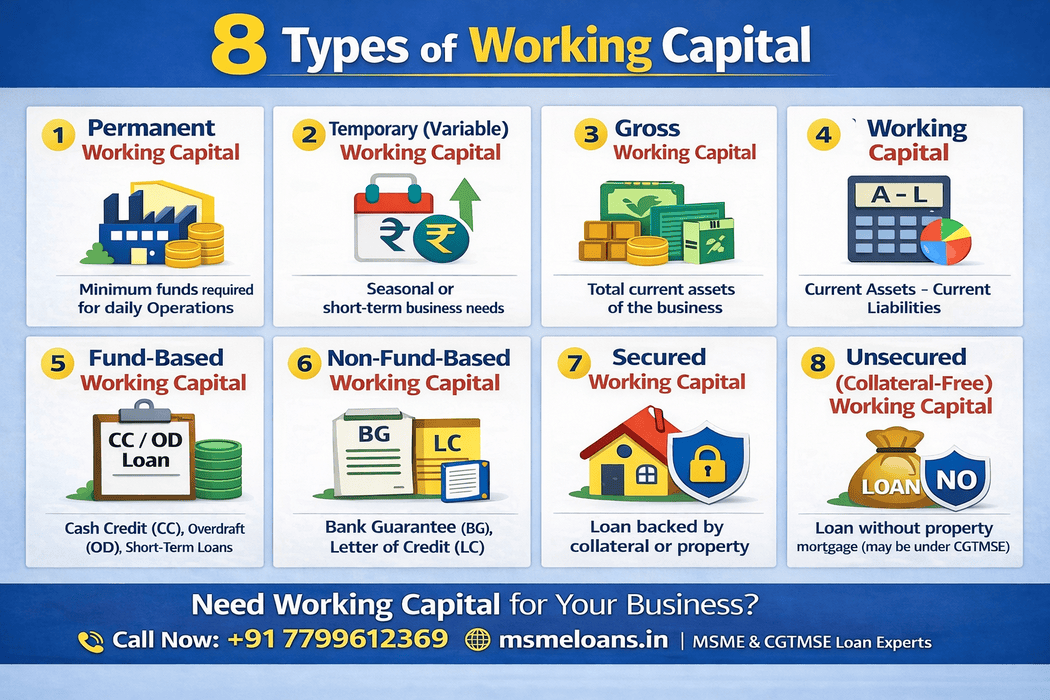

1. Permanent Working Capital

Permanent working capital refers to the minimum level of current assets a business must maintain to operate smoothly throughout the year. Even during low sales periods, a company needs funds to pay salaries, rent, electricity bills, and maintain inventory.

This type of working capital remains constant and does not fluctuate significantly. It is essential for long-term stability and business continuity.

Example: A manufacturing unit must always maintain a base stock of raw materials and pay fixed monthly salaries, regardless of sales volume.

2. Temporary (Variable) Working Capital

Temporary working capital is required to meet seasonal or temporary increases in business activity. It fluctuates depending on demand, production levels, and market conditions.

Businesses often require additional funds during peak seasons, festival sales, or when handling large orders.

Example: A retail business may require extra inventory during Diwali season, increasing short-term working capital needs.

3. Gross Working Capital

Gross working capital refers to the total current assets of a business. It includes:

- Cash and bank balance

- Inventory (stock)

- Accounts receivable

- Short-term investments

This concept focuses on the total funds invested in current assets without considering liabilities.

It represents the company’s ability to manage daily liquidity requirements.

4. Net Working Capital

Net working capital measures the financial health of a business and is calculated using the formula:

Net Working Capital = Current Assets – Current Liabilities

If current assets exceed current liabilities, the business has positive net working capital, indicating financial stability. Negative working capital may signal liquidity issues.

This measure is commonly used by banks to assess short-term solvency before approving working capital loans.

5. Fund-Based Working Capital

Fund-based working capital facilities involve the direct disbursement of funds by banks or financial institutions to support day-to-day business operations. In this structure, the lender provides actual cash flow support, and interest is charged on the amount utilized.

These facilities are widely used by MSMEs to manage operational expenses such as supplier payments, salary disbursement, inventory purchase, and short-term liquidity gaps.

Major types of fund-based working capital include:

- Cash Credit (CC): A revolving credit facility sanctioned against stock and receivables. The business can withdraw funds up to the sanctioned limit, and interest is charged only on the utilized amount. The limit is usually reviewed annually based on turnover and stock statements.

- Overdraft (OD): A flexible withdrawal facility linked to a current account. Businesses can withdraw more than the available balance up to the approved limit. It is suitable for managing temporary cash shortages.

- Short-Term Business Loan: A fixed tenure loan provided for operational needs. Unlike CC or OD, the amount is disbursed in lump sum and repaid through structured EMIs.

Fund-based facilities directly improve business liquidity and are commonly sanctioned based on turnover, financial statements, credit history, and working capital cycle.

For eligible MSMEs, these facilities may also be structured as collateral-free under CGTMSE coverage, subject to bank approval and credit assessment.

6. Non-Fund-Based Working Capital

Non-fund-based working capital does not involve direct fund disbursement but supports business operations through financial guarantees and trade instruments.

Common examples:

- Bank Guarantee (BG)

- Letter of Credit (LC)

- Bill Discounting

These facilities improve business credibility and facilitate trade transactions, especially in manufacturing and contracting businesses.

7. Secured Working Capital

Secured working capital loans require collateral such as property, fixed deposits, or other tangible assets. Since the bank has security coverage, interest rates may be comparatively lower.

However, businesses must pledge assets, which increases financial risk if repayment issues arise.

8. Unsecured (Collateral-Free) Working Capital

Unsecured working capital loans are provided without property mortgage. Eligible MSMEs can avail collateral-free funding under schemes like CGTMSE, subject to bank approval.

In such cases, banks may charge primary security such as stock and receivables but do not require additional collateral.

This option is suitable for growing businesses that prefer not to pledge personal or business assets.

9. Regular Working Capital

Regular working capital refers to the funds required for normal operational activities under stable business conditions. It is similar to permanent working capital but focuses on routine expenses rather than minimum liquidity.

It ensures that production, sales, and services continue without interruption.

10. Special Working Capital

Special working capital is required for specific situations such as launching a new product, entering a new market, executing a large contract, or expanding into new territory.

This type of capital is usually temporary but higher than normal operational needs.

Importance of Understanding Working Capital Types

Understanding the classification of working capital helps business owners:

- Choose appropriate loan structure

- Maintain healthy liquidity

- Avoid over-borrowing

- Improve financial planning

- Increase approval chances from banks

Banks assess both permanent and temporary working capital requirements before sanctioning limits. Proper financial documentation and cash flow planning improve eligibility.

Conclusion

Working capital is not just about borrowing funds; it is about maintaining the right balance between assets and liabilities. By understanding the different types of working capital — permanent, temporary, gross, net, fund-based, non-fund-based, secured, and unsecured — businesses can make informed financial decisions.

Choosing the correct structure ensures operational stability, growth potential, and long-term sustainability.