What is a Business Loan for Startup?

A business loan for startup is a type of financing provided to entrepreneurs who are establishing a new business. Unlike loans for existing businesses that are based on past financial performance, startup loans are evaluated based on the strength of the business idea, market potential, promoter background, and projected cash flow.

Banks assess whether the proposed business can generate enough revenue to repay the loan. If the project appears viable and well planned, financial institutions may approve funding even if the business has not yet started operations. You can also explore MSME loans for various business needs.

Startup loans are commonly used for:

- Purchasing machinery and equipment

- Setting up factories or commercial spaces

- Interior setup and infrastructure

- Working capital requirements

- Inventory purchase

- Business expansion and growth

What Types of Business Loans Are Available for Startups?

Startup businesses can access different types of financing depending on the nature of the project and capital requirement. The most common types include working capital loans, machinery loans, and project finance.

Term Loan for New Business

A term loan is used to finance fixed investments such as machinery, equipment, furniture, factory setup, or commercial infrastructure. These loans typically have repayment tenures ranging from 5 to 10 years depending on the size of the project.

Working Capital Loan for Startups

Working capital loans help businesses manage daily operational expenses such as raw materials, salaries, and inventory during early business stages.

Project Finance for New Businesses

Large startup projects such as manufacturing plants, hotels, hospitals, warehouses, and industrial facilities require structured project finance, where banks evaluate total project cost, expected revenue, and repayment ability.

Can Startups Get Business Loans Without Collateral?

Many entrepreneurs do not have sufficient assets to offer as collateral. In such cases, collateral-free loans are available under schemes like CGTMSE loan, depending on project feasibility and promoter profile.

Collateral-free loans are usually approved based on:

- Strong business model

- Promoter experience and background

- Financial projections

- Market demand

- Promoter contribution

Even without collateral, banks carefully evaluate the viability of the project before approving funding.

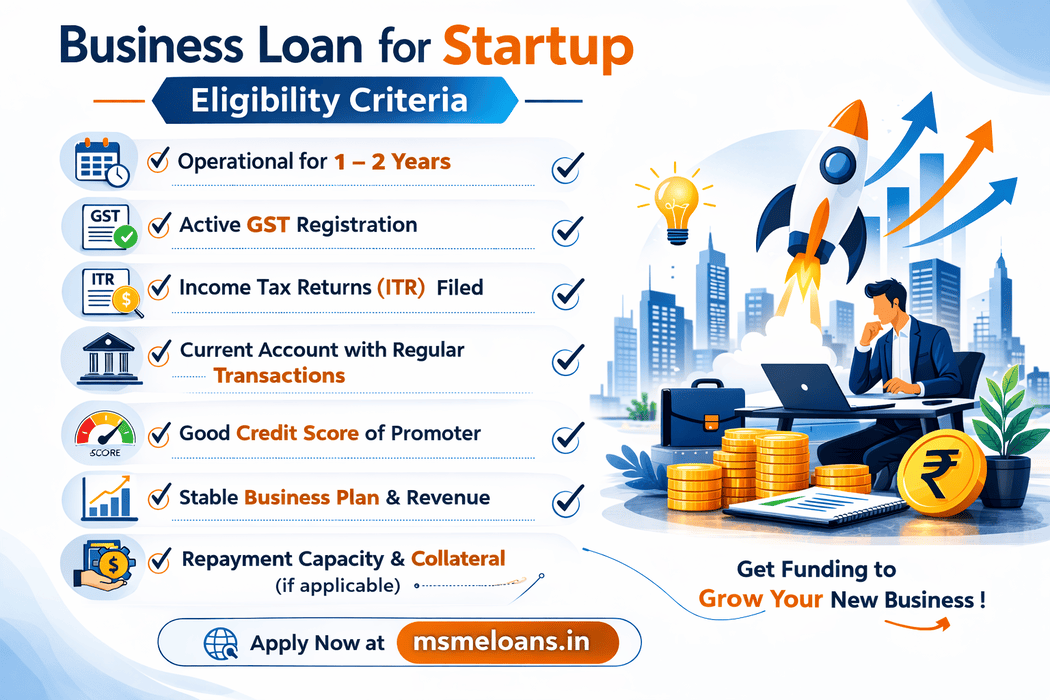

What is the Eligibility Criteria for Startup Business Loans?

To qualify for a startup business loan, lenders evaluate the financial stability and repayment capacity of the business.

- Business operational for at least 1–2 years (preferred)

- Active GST registration

- ITR filings available

- Regular bank transactions

- Good credit score (CIBIL)

- Stable revenue and repayment ability

Lenders analyze GST returns, bank statements, and ITR to assess financial strength. Learn more about MSME loan eligibility.

What Documents Are Required for a Startup Business Loan?

To apply for a startup loan, entrepreneurs must submit documents that help banks evaluate the project and promoter credibility.

- KYC documents (PAN, Aadhaar, address proof)

- Detailed Project Report (DPR) – view DPR guide

- Business plan with financial projections

- Bank statements

- Net worth statement

- Machinery or equipment quotations

- Business registration documents (if available)

Proper documentation improves loan approval chances significantly.

What Are the Latest Business Loan Interest Rates in India (April 2026)?

Business loan interest rates vary depending on lender, borrower profile, business turnover, and loan structure.

The following rates apply to businesses with 1–2 years of operations, GST registration, and good credit profile.

Public Sector Banks (PSU Banks)

| Bank | Interest Rate (% p.a.) |

|---|---|

| State Bank of India (SBI) | 9.10% – 11.65% |

| Punjab National Bank (PNB) | 9.60% – 12.50% |

| Bank of Baroda | 10.00% – 13.00% |

| Canara Bank | 9.20% – 12.00% |

| Indian Bank | 8.80% – 12.50% |

| UCO Bank | 10.00% – 13.00% |

Private Sector Banks

| Bank | Interest Rate (% p.a.) |

|---|---|

| HDFC Bank | 10.75% – 22.50% |

| ICICI Bank | 10.75% – 18.50% |

| Axis Bank | 16.00% onwards |

| Kotak Mahindra Bank | 9.50% – 30.50% |

| IDFC FIRST Bank | 12.99% onwards |

| YES Bank | 17.00% onwards |

NBFC Business Loan Interest Rates

| NBFC | Interest Rate (% p.a.) |

|---|---|

| Bajaj Finserv | 14.00% – 23.00% |

| Tata Capital | 12.00% onwards |

| Shriram Finance | 10.00% onwards |

| LendingKart | 17.00% onwards |

| FlexiLoans | 12.00% onwards |

| Muthoot Fincorp | 15.00% – 30.00% |

| Indifi Capital | 18.00% onwards |

| IIFL Finance | 16.00% onwards |

| Aditya Birla Finance | 13.00% onwards |

| UGRO Capital | 12.00% onwards |

Note: Interest rates vary based on credit score, turnover, loan amount, and lender policies.

What Are the Tentative Interest Rates for Startup Business Loans?

For completely new startups without financial history, interest rates are generally higher due to higher risk.

- Public Sector Banks (PSU): 10.50% – 14.00%

- Private Banks: 12.00% – 20.00%

- NBFCs: 14.00% – 28.00%

Explore collateral-free options under CGTMSE scheme.

Which Industries Commonly Receive Startup Funding?

Banks provide funding to startups across industries with strong demand and growth potential.

- Manufacturing units

- Restaurants and food businesses

- Healthcare facilities and hospitals

- Warehousing and logistics explore more on (warehouse loans)

- Retail businesses

How to Improve Startup Loan Approval Chances?

Since startups lack financial history, banks focus on project feasibility and promoter credibility.

- Prepare a strong and detailed DPR

- Maintain a good credit score

- Invest promoter contribution

- Choose the right lender

Improve approval chances with proper DSCR planning.

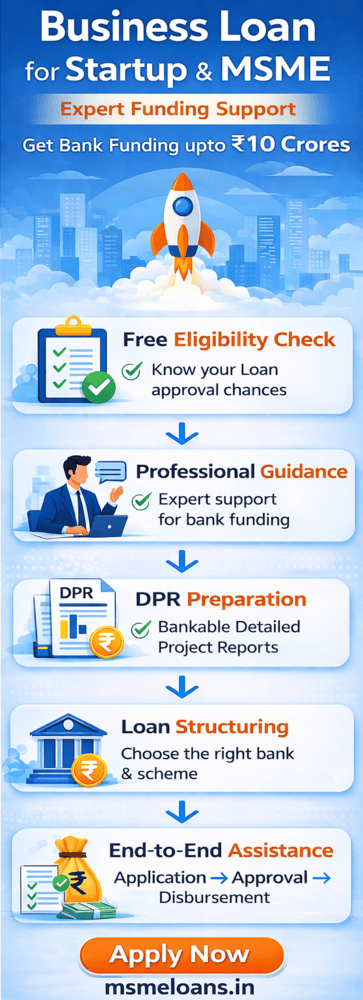

How Can You Apply for a Startup Business Loan?

- Prepare business plan and financial projections

- Estimate total project cost

- Submit required documents

- Apply to banks or NBFCs

- Complete verification and approval process

- Loan disbursement

Apply for Startup Business Loan

If you are planning to start a business and need funding, we help you structure your project and connect you with the right lenders.

Get expert assistance for startup loan approval today.

Conclusion

A business loan for startup can provide the capital required to turn your idea into a successful enterprise. With proper planning, strong financial projections, and the right guidance, startups can successfully secure funding and grow sustainably.