Greenfield vs Brownfield Project Differences Explained

When raising funds through project finance, understanding the difference between a greenfield project and a brownfield project is critical. Banks and financial institutions evaluate these two project types very differently in terms of risk, repayment capacity, promoter contribution, and documentation requirements.

If you are planning to set up a new industrial unit or expand an existing one, this guide explains how greenfield vs brownfield projects are treated in project finance.

What is a Greenfield Project in Project Finance?

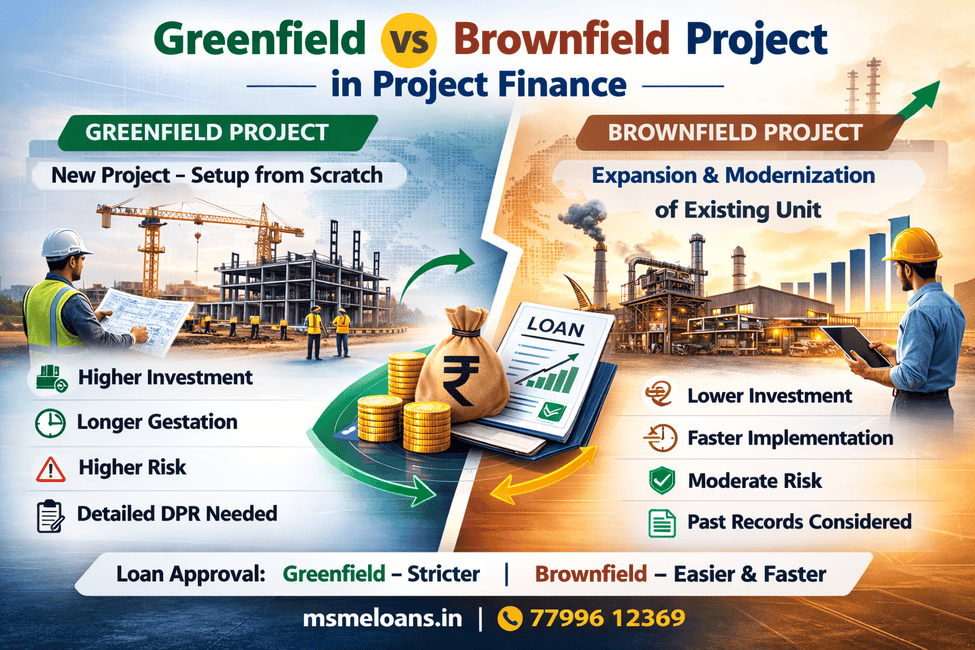

A greenfield project refers to setting up a completely new business unit from scratch. There is no existing infrastructure, operational history, or revenue track record. Everything — land, plant, machinery, utilities, workforce, and systems — must be developed fresh.

How Banks View Greenfield Projects:

- No past financial performance to evaluate

- Loan approval depends heavily on financial projections

- Higher risk due to uncertainty

- Strong emphasis on Detailed Project Report (DPR)

- Higher promoter contribution may be required

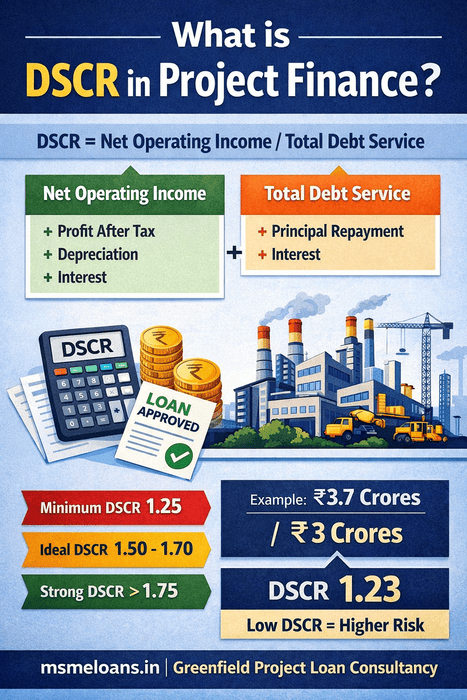

- Strict DSCR (Debt Service Coverage Ratio) assessment

Since there is no operating history, lenders rely on projected cash flows, industry viability, promoter background, and sensitivity analysis before sanctioning loans.

What is a Brownfield Project in Project Finance?

A brownfield project refers to expansion, modernization, or capacity enhancement of an existing operational business. The company already has revenue history, infrastructure, and financial statements.

How Banks View Brownfield Projects:

- Existing turnover and profit track record available

- Lower risk compared to greenfield

- Loan eligibility based on actual past performance

- Easier DSCR calculation using historical data

- Faster sanction process

Because lenders can assess repayment capacity based on real financial data, brownfield projects generally receive quicker approvals.

Greenfield Project – Advantages & Drawbacks

| Advantages | Drawbacks |

|---|---|

| Complete design freedom | Higher initial capital cost |

| Latest technology adoption | Longer project execution time |

| No legacy system constraints | Higher operational uncertainty |

| Better long-term scalability | No historical performance data |

| Efficient plant layout planning | Complex approvals & land acquisition |

| Easier sustainability integration | Higher risk during initial years |

| Modern safety standards from start | Longer break-even period |

Brownfield Project – Advantages & Drawbacks

| Advantages | Drawbacks |

|---|---|

| Lower initial investment | Limited structural flexibility |

| Faster implementation | Integration with old systems |

| Existing infrastructure available | Environmental cleanup may be required |

| Proven operational history | Space limitations |

| Reduced project uncertainty | Upgradation challenges |

| Quicker time to market | Possible hidden repair costs |

| Lower execution risk | Limited innovation scope |

Greenfield Project – Finance Perspective

| Advantages (Finance View) | Drawbacks (Finance View) |

|---|---|

| High long-term growth potential | Higher promoter contribution (25–35%) |

| Scalable revenue projections | Loan approval stricter |

| Custom capital structuring possible | DSCR based only on projections |

| Potential higher ROI in long term | Higher risk perception by lenders |

| Eligible under MSME & CGTMSE schemes | Longer moratorium may be required |

| Suitable for large industrial expansion | Detailed DPR mandatory |

Brownfield Project – Finance Perspective

| Advantages (Finance View) | Drawbacks (Finance View) |

|---|---|

| Easier credit appraisal | Limited large-scale growth |

| Historical financials available | May inherit old liabilities |

| Faster loan processing | Asset depreciation considerations |

| Better DSCR visibility | Possible modernization cost |

| Lower promoter margin requirement | Capacity constraints |

| Lower lender risk perception | Limited collateral enhancement |

Promoter Contribution in Greenfield vs Brownfield Projects

In project finance, promoter contribution plays a major role. For greenfield projects, banks may require 25%–35% margin money due to higher risk. In brownfield projects, margin requirements may be comparatively lower because the business already demonstrates repayment capability.

DSCR Evaluation Differences

For greenfield projects, DSCR is calculated purely on projected financials. Therefore, realistic revenue assumptions and properly structured cost estimates are critical.

For brownfield projects, banks analyze past 2–3 years financial statements and combine them with expansion projections to calculate repayment capacity.

Which Project Type is Easier to Finance?

From a lender’s perspective:

- Brownfield projects are generally easier to finance due to existing financial performance.

- Greenfield projects require strong financial structuring, detailed DPR, industry experience, and realistic projections.

However, well-structured greenfield proposals with proper documentation can still secure funding under MSME schemes and project finance models.

Role of CGTMSE in Greenfield and Brownfield Projects

Both greenfield and brownfield MSME projects can be financed under CGTMSE (Credit Guarantee Scheme), provided eligibility conditions are met. However, greenfield cases undergo deeper scrutiny due to the absence of operating history.

Final Thoughts

Understanding the difference between greenfield vs brownfield project in project finance helps entrepreneurs plan capital structure, promoter contribution, and loan strategy effectively. While brownfield projects offer faster approvals, greenfield projects provide long-term growth opportunities if structured properly.

Proper DPR preparation, financial modeling, and documentation alignment with bank credit policies significantly improve approval chances for both project types.