Preparing a bankable Detailed Project Report (DPR) is the most critical step in securing a Greenfield Project Loan. Whether you are setting up a new manufacturing unit, warehouse, hotel, hospital, or food processing plant, banks evaluate your DPR before sanctioning project finance.

A professionally structured DPR improves loan approval chances, strengthens banker confidence, and ensures faster sanction.

What is a DPR in Greenfield Project Finance?

A Detailed Project Report (DPR) is a comprehensive document submitted to banks explaining:

- Project feasibility

- Technical viability

- Market demand

- Financial sustainability

- Repayment capacity

Banks use the DPR to evaluate the long-term viability and risk of funding the project.

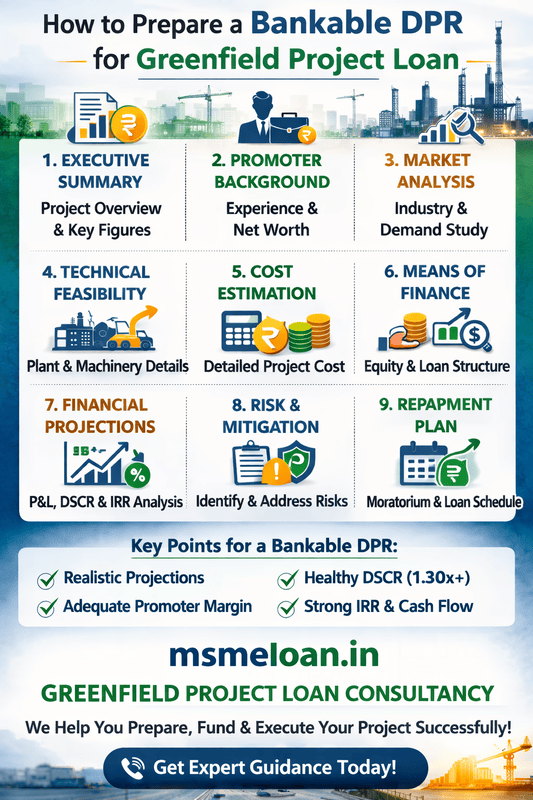

Structure of a Bankable DPR for Greenfield Project

1. Executive Summary

This is the first section bankers read. It should include:

- Project name and location

- Industry sector

- Total project cost

- Promoter contribution

- Term loan requirement

- Debt–Equity ratio

- Project IRR

- Average DSCR

- Break-even year

Keep this section clear, professional, and data-driven.

2. Promoter Profile & Background

Banks finance promoters, not just projects. Include:

- Educational background

- Industry experience

- Existing business performance

- Net worth statement

- Income Tax Returns (last 3 years)

- CIBIL score

If the promoter lacks experience, justify the project with technical team support.

3. Industry & Market Analysis

This section must demonstrate demand viability. Include:

- Industry overview

- Market size and growth rate

- Demand–supply gap

- Target customer segment

- Competitor analysis

- Pricing strategy

Avoid unrealistic revenue assumptions.

4. Technical Feasibility

Banks verify whether the project can be practically executed. Include:

- Location advantages

- Land ownership or lease details

- Building plan and layout

- Machinery details with quotations

- Installed production capacity

- Manufacturing process flow

- Raw material availability

- Power and water requirements

Attach machinery quotations wherever possible.

5. Project Cost Estimation

Clearly break down total project cost into:

- Land cost

- Building & civil construction

- Plant & machinery

- Electrical installation

- Preliminary & pre-operative expenses

- Contingency provision

- Margin for working capital

- Interest During Construction (IDC)

Total Project Cost = Fixed Capital + Working Capital Margin

6. Means of Finance

Explain funding structure clearly:

- Promoter contribution (normally 25%–35%)

- Term loan

- Subsidy (if applicable)

- Unsecured loans (if any)

Maintain a realistic Debt–Equity Ratio (generally 2:1).

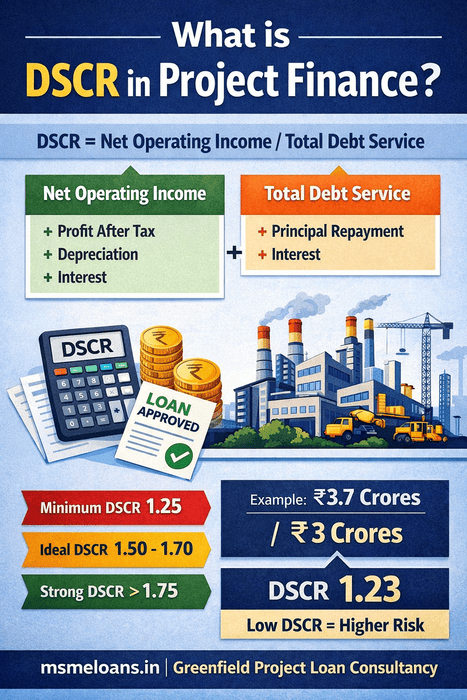

7. Financial Projections (Most Critical Section)

This section determines loan approval. Prepare:

- Projected Profit & Loss (7–10 years)

- Projected Balance Sheet

- Cash Flow Statement

- DSCR calculation

- Break-even analysis

- IRR calculation

- Sensitivity analysis

Minimum Banking Standards:

- Average DSCR: 1.30x – 1.50x

- Project IRR greater than loan interest rate

- Positive operational cash flow

Avoid overestimating sales projections.

8. Moratorium & Repayment Structure

- Construction period timeline

- Moratorium period (usually 12–24 months)

- Loan tenure (7–10 years normally)

- Structured repayment aligned with cash flow

Repayment schedule must match realistic project performance.

9. Risk Analysis & Mitigation

Include a clear risk assessment section:

- Market risk

- Raw material price risk

- Operational risk

- Competition risk

- Regulatory risk

Mention mitigation strategies for each identified risk.

Common Mistakes in DPR Preparation

- Inflated revenue projections

- Ignoring working capital requirements

- Incorrect DSCR calculations

- No contingency provision

- Weak promoter justification

- Absence of sensitivity analysis

These errors often result in loan rejection.

Documents Required Along with DPR

- Land documents

- Building approvals

- Machinery quotations

- Net worth certificate

- Income Tax Returns

- Bank statements

- Pollution clearance (if required)

- Projected CMA data

What Makes a DPR Truly Bankable?

- Realistic financial projections

- Healthy and consistent DSCR

- Adequate promoter margin

- Strong project IRR

- Justified market demand

- Clear risk mitigation strategy

Conclusion

A Greenfield Project Loan requires structured planning, accurate financial modelling, and professional documentation. A properly prepared DPR significantly improves loan approval chances and enhances banker confidence.

If you are planning a new industrial or infrastructure project, ensure your DPR meets banking standards before submission.