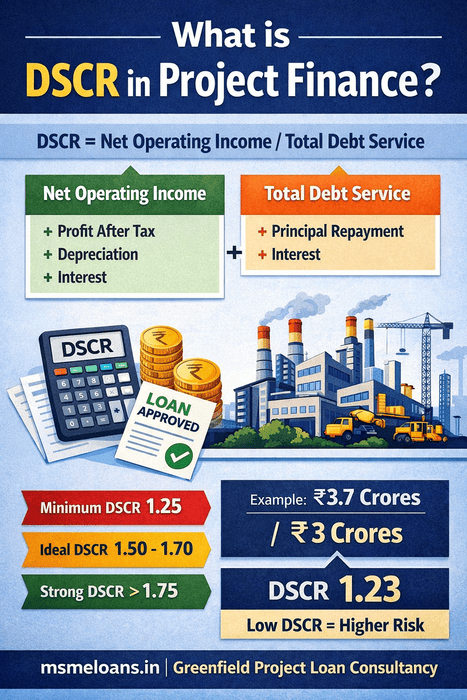

What is DSCR in Project Finance?

DSCR (Debt Service Coverage Ratio) measures the ability of a project to generate sufficient cash flow to repay its loan obligations.

DSCR requirement one of the most critical financial ratios evaluated by banks while sanctioning a

Greenfield Project Loan for MSME

.

DSCR Formula

DSCR = Net Operating Income / Total Debt Service

- Net Operating Income = Profit After Tax + Depreciation + Interest

- Total Debt Service = Annual Principal Repayment + Interest

Minimum DSCR Required by Banks

- Minimum acceptable: 1.25

- Comfortable range: 1.50 – 1.70

- Strong project rating: Above 1.75

For Greenfield projects above ₹10 Crores, banks generally prefer an average DSCR of at least 1.50 for stable repayment capacity.

Projects structured under

Machinery Loan for MSME

or full-scale

Greenfield Project Finance

must maintain comfortable repayment ratios to improve sanction chances.

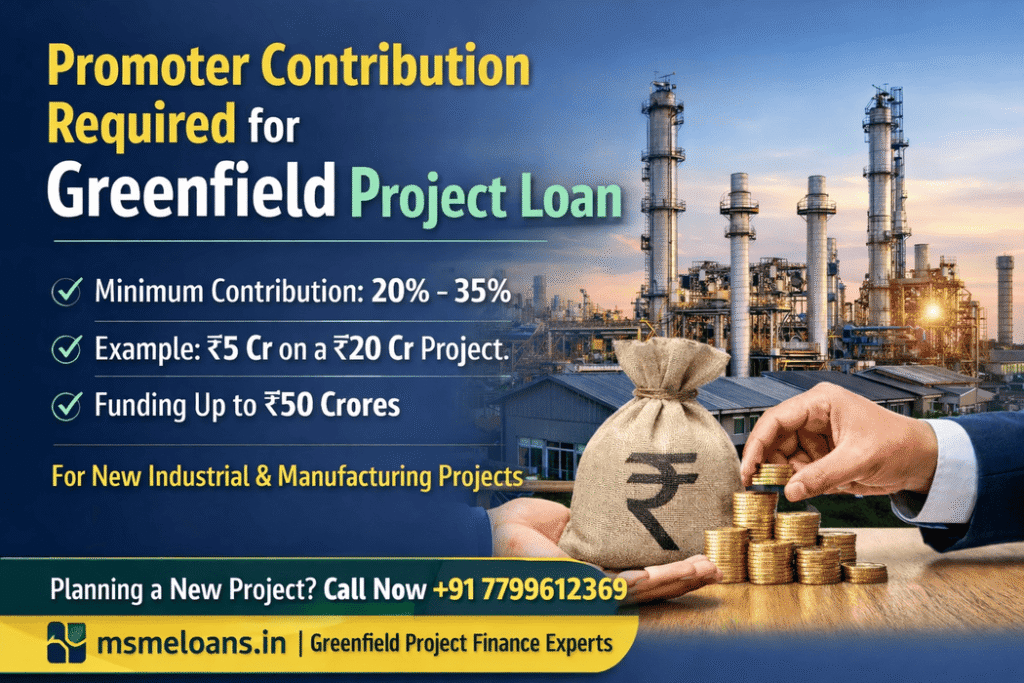

Practical Example – ₹20 Crore Greenfield Project

Project Cost: ₹20 Crores

Promoter Contribution (25%): ₹5 Crores

Bank Term Loan (75%): ₹15 Crores

Large projects may also combine term loans with

Working Capital Loan

facilities to manage operational cash flow efficiently.

Assume the loan tenure is 10 years at 10% interest.

Annual Loan Obligation

- Annual Principal Repayment: ₹1.5 Crores

- Annual Interest (approx first year): ₹1.5 Crores

- Total Annual Debt Service: ₹3 Crores

Projected Operational Performance

- Projected EBITDA: ₹4.5 Crores

- Depreciation: ₹1 Crore

- Interest: ₹1.5 Crores

- Profit After Tax (approx): ₹1.2 Crores

Net Operating Income = PAT + Depreciation + Interest

= 1.2 + 1 + 1.5 = ₹3.7 Crores

DSCR = 3.7 / 3 = 1.23

In this case, DSCR of 1.23 is weak and may not satisfy bank comfort level.

Banks may require additional collateral or structured guarantees such as

CGTMSE Loan support

in eligible cases.

Improved Scenario

If the promoter increases contribution or extends tenure, annual repayment reduces.

Assume revised annual debt service reduces to ₹2.5 Crores.

Revised DSCR = 3.7 / 2.5 = 1.48

Now the DSCR is close to 1.5, which is acceptable for most banks.

Why DSCR is Critical in Greenfield Projects

- No past financial history

- Banks rely heavily on projections

- Cash flow accuracy determines sanction

- Over-projection may lead to rejection

A well-structured Detailed Project Report (DPR) and realistic CMA projections significantly improve sanction probability for large

Greenfield Project Loans

.

Conclusion

For MSME Greenfield Projects seeking funding up to ₹50 Crores, maintaining an average DSCR of 1.5 or above is crucial.

Professional financial structuring, optimized tenure planning, and realistic revenue projections play a key role in successful project finance approval.