Many business owners apply for a working capital loan for MSME to manage daily operational expenses such as supplier payments, salaries, inventory purchases, and utility bills. However, one common question among entrepreneurs is how banks actually calculate the working capital limit for a business. Understanding the calculation method can help businesses prepare better financial records

and improve their chances of loan approval.

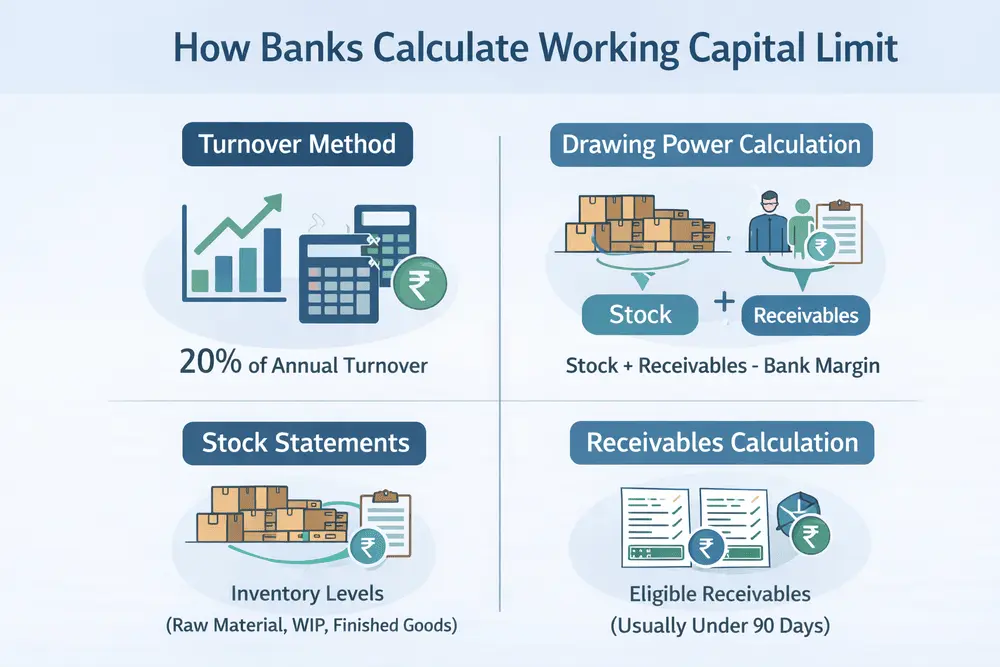

Banks evaluate the working capital requirement based on the business turnover, operating cycle, inventory levels, receivables, and overall financial stability. The two most common methods used by banks are the Turnover Method and the Drawing Power Method.

1. Turnover Method (For MSME Businesses)

The turnover method is commonly used for small and medium enterprises when calculating working capital requirements. Under this method, banks generally estimate the working capital limit as a percentage of the projected annual turnover of the business.

As per RBI guidelines for MSME financing, banks may consider around

20% of the projected annual turnover as the working capital requirement.

Example:

- Projected annual turnover: ₹5 Crore

- Working capital requirement (20%): ₹1 Crore

In this case, the bank may sanction a working capital limit close to ₹1 Crore depending

on the financial strength of the business and the promoter’s contribution.

2. Drawing Power Method

The drawing power method is used when working capital facilities such as

cash credit (CC) are sanctioned against stock and receivables. In this method, the bank calculates how much money the borrower can withdraw based on the value of inventory and outstanding receivables.

The basic formula used by banks is:

Drawing Power = (Stock + Receivables) – Bank Margin

Banks usually apply a margin of around 20% to 30% depending on

the industry and risk profile.

Example:

- Stock value: ₹80 Lakhs

- Receivables: ₹40 Lakhs

- Total: ₹1.2 Crore

- Bank margin (25%): ₹30 Lakhs

- Eligible drawing power: ₹90 Lakhs

This means the borrower can utilize up to ₹90 Lakhs from the sanctioned

working capital limit.

3. Role of Stock Statements

For businesses operating under cash credit facilities, banks require regular stock statements to monitor the value of inventory and receivables. These statements are usually submitted monthly.

Stock statements help the bank ensure that the working capital loan is properly secured against business assets such as raw materials, finished goods, and trade receivables.

If the stock value decreases significantly, the drawing power may

also reduce accordingly.

4. Receivables Calculation

Receivables represent the money owed to the business by its customers.

Banks include receivables while calculating drawing power, but only

those receivables that fall within a certain credit period.

Typically, banks consider receivables that are less than

90 days old. Older receivables are usually excluded

from the calculation because they are considered higher risk.

Businesses with strong receivable management and shorter credit cycles

generally qualify for higher working capital limits.

Factors Banks Consider Before Sanctioning Working Capital Limit

- Annual business turnover

- Profitability and financial statements

- Stock and inventory levels

- Receivable cycle

- Bank transaction history

- CIBIL score of promoters

- GST returns and tax compliance

Maintaining proper financial records and consistent banking transactions

can significantly improve the chances of getting a higher working capital

limit from banks.

Conclusion

Banks calculate working capital limits using structured financial methods

such as turnover analysis and drawing power calculations. These methods

help lenders ensure that businesses receive funding based on their actual

operational requirements and repayment capacity.

If your business requires funds to manage inventory, supplier payments,

or operational expenses, understanding the calculation process of a

working capital loan for MSME

can help you prepare better and secure the right financing solution.