What is Promoter Contribution in Project Finance?

Promoter contribution refers to the amount of capital that the business owner must invest in a project before a bank sanctions a loan.

In a

Greenfield Project Loan for MSME

, banks expect the promoter to bring a certain percentage of the total project cost as margin money.

Banks do not fund 100% of a new project. Promoter investment demonstrates financial commitment, reduces lender risk, and improves overall loan approval probability.

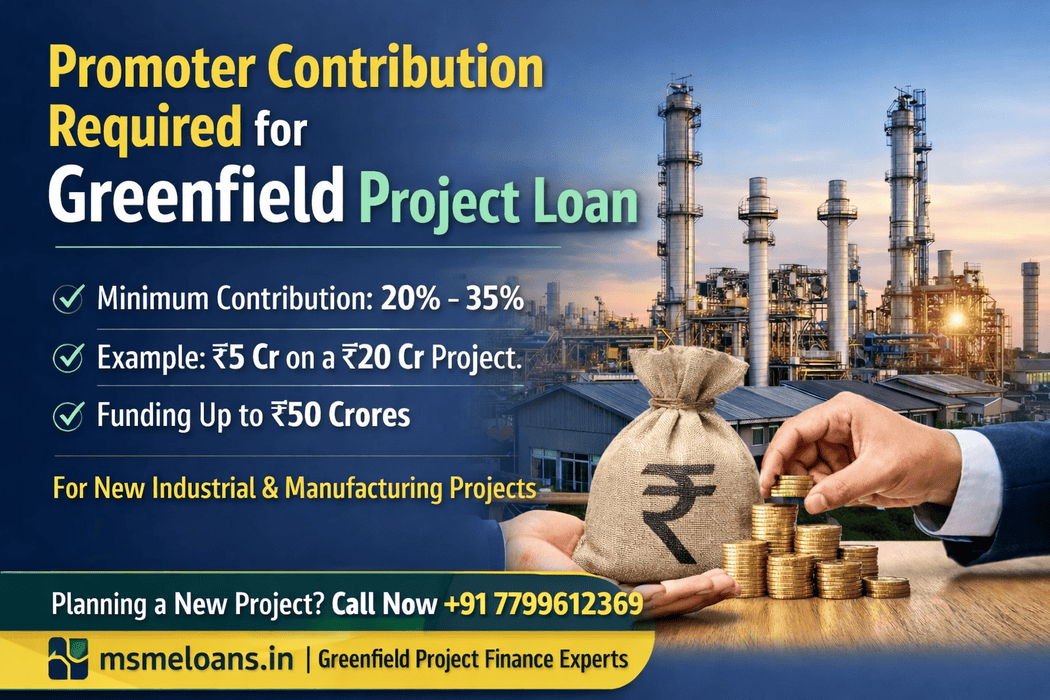

Minimum Promoter Contribution Required by Banks

- Small & Medium Projects (₹50 Lakhs – ₹5 Crores): 20% – 25%

- Mid-Sized Projects (₹5 Cr – ₹10 Cr): 25% – 30%

- Large Projects (₹10 Crores+): 25% – 35%

- High-Risk or New Promoters: Higher contribution may be required

For example, in a ₹20 Crore Greenfield project:

- Total Project Cost: ₹20 Crores

- Promoter Contribution (25%): ₹5 Crores

- Bank Term Loan (75%): ₹15 Crores

The final margin requirement depends on promoter net worth, industry risk, collateral coverage, and projected cash flows.

Why Banks Require Promoter Contribution

- Ensures promoter skin in the game

- Reduces bank’s financial exposure

- Improves project viability perception

- Enhances long-term repayment stability

Higher promoter contribution may also help negotiate better interest rates and repayment terms under structured

Greenfield Project Finance

.

Can Promoter Contribution Be in the Form of Land?

Yes. In many cases, the market value of industrial land already owned by the promoter may be treated as part of promoter contribution, subject to independent bank valuation and legal verification.

However, only the accepted valuation (not purchase price) is considered by the bank.

How to Arrange Promoter Contribution?

- Personal savings or retained earnings

- Capital infusion from partners or shareholders

- Equity investment

- Sale of non-core assets

- Unsecured loans from family (subject to bank approval norms)

What Happens If Promoter Contribution is Low?

- Reduction in sanctioned loan amount

- Higher collateral requirement

- Stricter loan conditions

- Delay or rejection of proposal

Proper financial planning and realistic projections improve approval chances significantly.

Promoter Contribution vs Working Capital Margin

Promoter contribution applies to long-term project assets such as land, building, plant & machinery.

Working capital margin applies to day-to-day operational funding requirements.

For operational funding needs, promoters may separately explore

Working Capital Loan

facilities.

Conclusion

For MSME Greenfield Projects seeking funding up to ₹50 Crores, maintaining promoter contribution of at least 20%–30% significantly improves bank sanction probability.

If you are planning a new industrial setup or expansion, structured planning under

Greenfield Project Loan for New Business

can improve approval speed and funding flexibility.