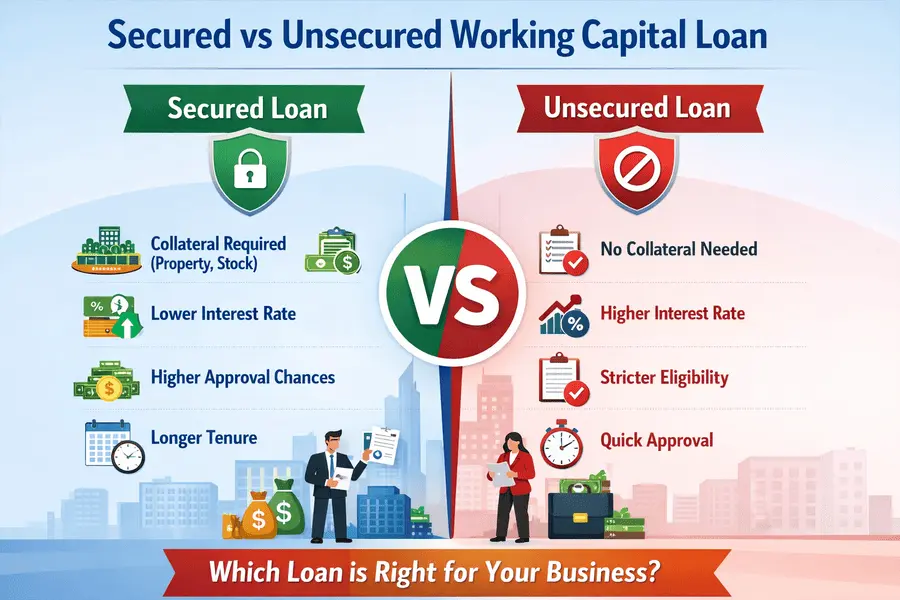

Working capital loans help businesses manage temporary liquidity gaps. However, lenders usually offer two main types of facilities — secured working capital loans and unsecured working capital loans. Each option has different eligibility requirements, interest rates, and approval chances.

What is a Secured Working Capital Loan?

A secured working capital loan is a credit facility where the borrower provides collateral or security to the lender. This security can include business property, inventory, receivables, or other business assets. Because the lender has collateral protection, secured loans usually have lower interest rates and higher approval chances.

Banks commonly provide secured working capital facilities in the form of cash credit (CC), overdraft (OD), and working capital term loans. These facilities are often linked to the business’s stock levels and receivables.

- Lower interest rates compared to unsecured loans

- Higher loan limits

- Better approval chances

- Longer repayment tenure

What is an Unsecured Working Capital Loan?

An unsecured working capital loan for msme allows businesses to borrow funds without pledging property or assets as collateral. These loans are generally offered by banks and NBFCs based on the business’s financial performance, turnover, bank transactions, and credit score.

Many MSMEs can also access collateral-free funding through the

CGTMSE loan scheme.Under this government-backed program, banks receive guarantee coverage,

which allows them to provide working capital loans without requiring

property mortgage from eligible businesses.

Businesses with strong financial records, healthy bank statements, and good

promoter contribution and credit profile have better chances of approval.

Since lenders take higher risk when providing unsecured loans, they apply stricter eligibility criteria. Businesses with strong financial records, healthy bank statements, and good CIBIL scores have better chances of approval.

- No collateral required

- Faster loan processing

- Minimal documentation

- Higher interest rates compared to secured loans

Key Differences Between Secured and Unsecured Working Capital Loans

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral | Property, stock, or receivables required | No collateral required |

| Interest Rate | Lower (typically 8.5% – 12%) | Higher (typically 11% – 24%) |

| Approval Chances | Higher approval rate | Lower approval rate |

| Loan Amount | Higher loan limits | Usually smaller limits |

| Processing Time | Slightly longer due to collateral verification | Faster approval in many cases |

Which Option is Better for MSMEs?

For most businesses, secured working capital loans are usually the preferred option because they offer lower interest rates and higher loan limits. Banks feel more comfortable lending when the facility is backed by collateral such as property, stock, or receivables.

However, unsecured loans can still be useful for businesses that need quick funding and do not want to pledge assets. These loans are commonly used for short-term working capital requirements.

Important Note for Business Owners

Unsecured working capital loans often have stricter eligibility requirements. If a business has irregular bank transactions, low profitability, poor GST compliance, or a weak credit score, lenders may reject the application. In comparison, secured facilities usually have a higher approval rate because the lender has collateral protection.

Many MSMEs therefore choose a secured working capital facility such as cash credit or overdraft to ensure stable financing and lower borrowing costs.

Conclusion

Both secured and unsecured working capital loans play an important role in business financing. The right choice depends on the financial profile of the business, the urgency of funds, and the availability of collateral. Businesses with strong financial discipline and collateral support generally benefit from lower interest rates and higher limits through secured facilities.

If your business needs flexible funding to manage operational expenses, inventory purchases, or supplier payments, understanding the structure of a working capital loan for MSME can help you choose the right financing option.