The SATAT (Sustainable Alternative Towards Affordable Transportation) scheme, launched by the Ministry of Petroleum and Natural Gas in 2018, has fundamentally changed the bankability calculus for Compressed Bio-Gas (CBG) projects in India.

For years, CBG was seen as a promising but financially opaque sector — good technology, poor financing. SATAT changed that. Today, a well-structured CBG project under SATAT can achieve financial closure with a combination of bank debt, private equity, and green financing. Here is a detailed breakdown of exactly why.

1. Guaranteed Offtake — The Single Biggest Bankability Driver

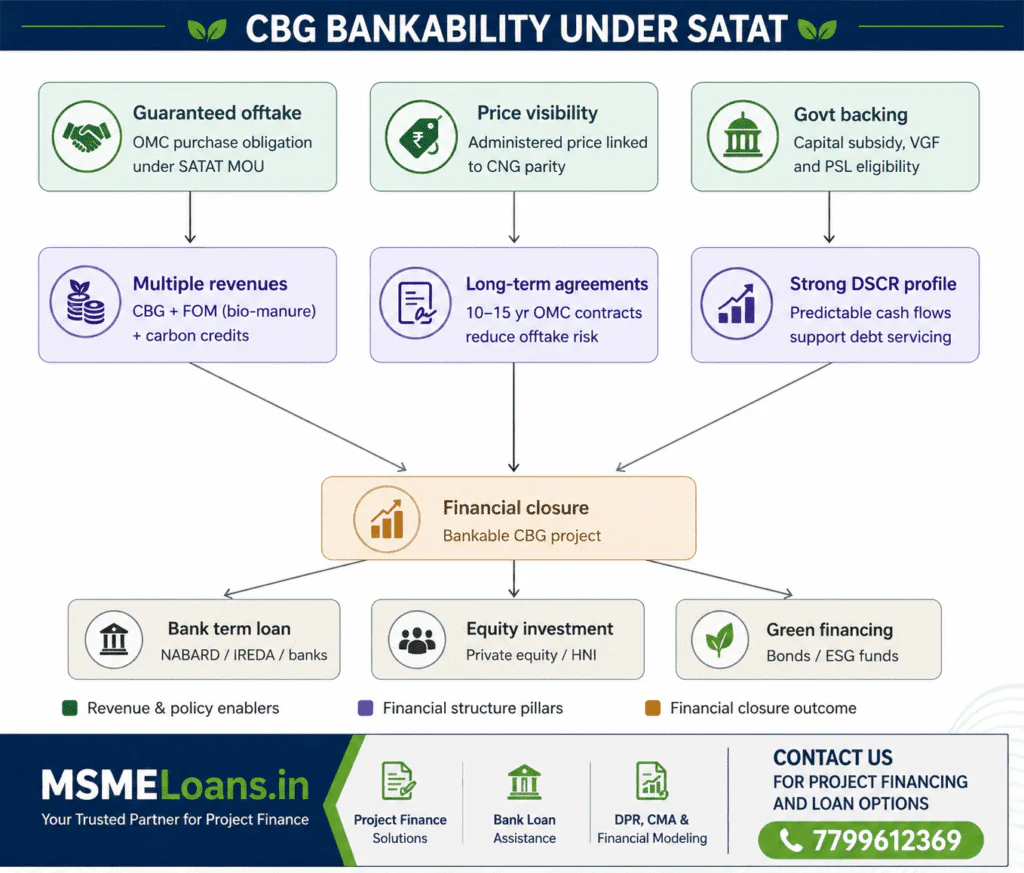

The core reason CBG projects are financeable today is that SATAT mandates Oil Marketing Companies (OMCs) — IOCL, BPCL, and HPCL — to sign offtake agreements with registered CBG producers. This removes the single biggest risk lenders face: “Who will buy the gas?”

Without SATAT, a CBG developer would need to independently find buyers in a nascent market. With SATAT, the buyer is a government-backed OMC with a long-term purchase obligation. This single feature converts a speculative project into an infrastructure-style investment.

For lenders: The SATAT offtake agreement functions like a Power Purchase Agreement (PPA) in the solar sector — it provides a contracted revenue stream that forms the foundation of the entire debt repayment model.

2. Price Visibility — Lenders Can Finally Model Cash Flows

SATAT provides an administered pricing mechanism where CBG is priced with reference to CNG parity. This means:

- Revenue per kg of CBG is predictable over the project life

- Financial models can be built with reasonable price escalation assumptions

- Banks can stress-test cash flows against multiple price scenarios

- Sensitivity analysis becomes credible and defensible

Without price visibility, no lender will commit to a 10–12 year term loan. SATAT provides exactly that visibility — and that is what makes the Detailed Project Report (DPR) bankable.

3. Multiple Revenue Streams Strengthen the DSCR

A well-structured CBG project under SATAT does not rely on a single revenue line. It generates income from three distinct sources:

- CBG sales to OMCs — primary revenue (typically 70–80% of total project revenue)

- Fermented Organic Manure (FOM) — byproduct sold to farmers and agri-businesses (10–15%)

- Carbon credits — under Voluntary Carbon Standards (VCS) or India’s Carbon Credit Trading Scheme (5–15%)

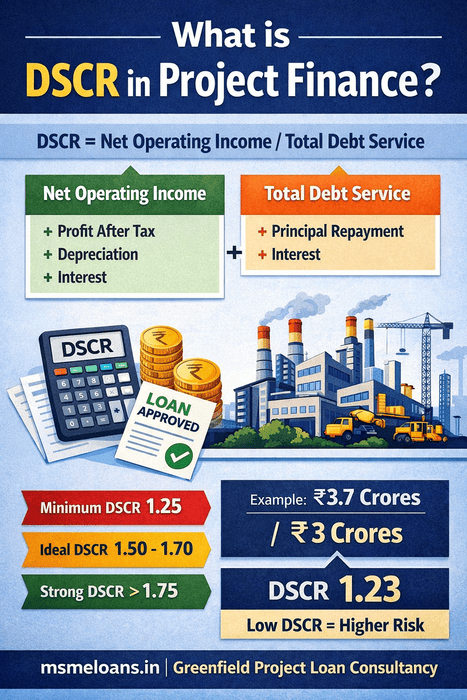

This blended revenue model significantly improves the Debt Service Coverage Ratio (DSCR). Lenders typically require a minimum DSCR of 1.2x–1.3x for infrastructure projects. Well-structured CBG projects with all three revenue streams can achieve a DSCR of 1.4x–1.8x — comfortably within bankable territory.

Advisor’s note: Carbon credit revenue is still underutilised by most CBG developers. Properly structured, it can add 5–15% to total project revenue and push marginal projects into bankable DSCR territory.

4. Government Support Reduces the Cost of Capital

SATAT-registered projects qualify for multiple layers of government financial support that directly improve project economics:

- Capital subsidy under MNRE’s biogas development programs

- Viability Gap Funding (VGF) for projects that require additional financial support to achieve viability

- Priority Sector Lending (PSL) classification — enables commercial banks to lend at concessional interest rates

- NABARD financing — long-tenure, low-cost debt for rural and agricultural energy projects

- IREDA financing — dedicated renewable energy lending at competitive rates

This combination reduces the effective cost of capital significantly, improving the Internal Rate of Return (IRR) for equity investors and making the overall project economics more attractive for all stakeholders.

5. Long-Term Agreements Mirror Classic Infrastructure Project Finance

SATAT offtake agreements typically run for 10–15 years. This long tenure is critical because it:

- Matches the loan repayment tenure of a typical term loan (8–12 years)

- Provides revenue visibility well beyond the loan repayment period

- Reduces refinancing risk at the end of the debt tenure

- Enables lenders to model full loan recovery comfortably within the contract period

- Provides a residual revenue period post-debt repayment — improving equity IRR

This is the classic project finance structure — long-dated contracted revenue matched against long-dated debt — that banks and infrastructure funds have been financing for decades in sectors like roads, ports, and power. CBG under SATAT now fits the same template.

6. What Banks and Lenders Still Want to See

Despite the structural advantages SATAT provides, lenders will still conduct rigorous due diligence. A bankable CBG project must demonstrate:

- Credible feedstock supply agreement — minimum 3–5 year supply contract with quantity and price certainty

- Proven technology — from an established EPC vendor with a track record of operating plants

- Experienced project team — management capability to execute and operate the plant

- Conservative DPR assumptions — lenders will stress-test; build in realistic capacity utilisation and feedstock cost escalation

- Adequate promoter equity — typically 25–30% of total project cost as promoter contribution

- Environmental clearances — all regulatory approvals in place or clearly on track

Key insight: The most common reason CBG projects fail at financial closure is not the technology or the market — it is an inadequately prepared DPR with over-optimistic assumptions. Lenders have seen enough projects to know when numbers have been reverse-engineered to show viability.

7. The SATAT-Solar Parallel — Why This Matters for Investors

In 2010, solar power in India faced exactly the same financing challenges CBG faced until recently — promising technology, uncertain buyers, no price framework, and skeptical lenders. The Jawaharlal Nehru National Solar Mission (JNNSM) changed that by providing a policy framework that gave lenders and investors the confidence to commit capital.

SATAT is doing the same for CBG. The scheme provides the three things every project finance lender needs:

- A creditworthy buyer (OMCs)

- A long-term price framework (CNG parity pricing)

- Government backing (subsidies, PSL, NABARD/IREDA access)

The Indian solar sector grew from near zero to over 70 GW in 15 years once these three elements were in place. CBG has the same structural tailwinds today.

The Project Finance Advisor’s Conclusion

SATAT has done for CBG what the JNNSM did for solar — transformed a technically viable but financially opaque sector into a bankable asset class. The combination of guaranteed offtake, price visibility, government support, multiple revenue streams, and long-term contracts makes CBG one of the most structurally sound green energy investment opportunities in India today.

The projects that will achieve financial closure fastest are those where the promoter arrives with a well-prepared DPR, a clear feedstock supply plan, and an advisor who understands how to package the SATAT framework into a lender-ready financing structure.

If you are a developer, investor, or lender evaluating a CBG project under SATAT, I would be happy to discuss how to structure it for financial closure.

About the Author

Raja venkat is a Project Finance Advisor specialising in CBG, renewable energy, and green infrastructure projects in India.